Papandreou’s government passes the first austerity hurdle

Against a backdrop of violent demonstrations, George Papandreou’s PASOK government won a first vote on Medium-Term Fiscal Strategy (MTFS) on Wednesday 29. The vote brought a sign of relief but the focus now shifts to the second hurdle: the associated implementation law which is expected today at midday local time (11 CET). If all goes well, the Eurogroup will then meet on July 3 to finalise a new 3-year programme for Greece involving the private sector. This would effectively remove the need for Greece to access bonds markets before 2015. If the Greek parliament changes significantly the terms of the implementation law (a scenario to which we attach a nonnegligible probability), the risk is that EU/IMF would block the much needed next €12bn tranche. The political vacuum would likely trigger a general election in September and the EU/ECB would have to take aggressive action to stem contagion.

As expected, Papandreou obtained a relatively narrow majority on the MTFS, with 155 votes to 138 (5 abstentions). The MTFS includes €28bn of additional austerity measures for 2011-2012 as well as an accelerated privatisation plan. However, Greece has far from adopted the austerity package. Indeed, the Parliament votes again on Thursday on measures to implement the MTFS.

IMF/EU will only disburse if the implementation law does not lose its inner significance. The Parliaments agreed yesterday on the package as a whole. The risk is now that it modifies substantially some implementation measures, as a result of which the modified MTFS could not meet IMF/EU requirements. The IMF made it clear that the July tranche to Greece can only be disbursed if 1) Greece adopts the austerity package 2) the EU provides concrete assurances that it will continue to provide funding to Greece as stipulated under the EU/IMF adjustment programme. In other words, only after the MTFS is approved can the Troika officially put forward a medium-term funding plan for Greece involving private creditors, through to 2014. And only once Greece is funded for at least the next twelve months will the IMF give its official consent to its share of the quarterly disbursement (€3.3bn over €12bn). A decision from the EU on Greece’s medium-term funding could be reached at the Eurogroup Meeting on Sunday 3 July, rather than on 11 July (as currently scheduled). That would then clear the way for the IMF to authorise its share of the quarterly disbursements too.

No plan B Although not the most likely outcome, significant changes in the MTFS would throw the country in a political vacuum and pave the way for anticipated elections. Indeed, Euro area leaders warned that there was no plan B in case the package was not approved. As the centre-right opposition party New Democracy would be well placed to win the new election and as it is not opposed to austerity per se but wants a ‘different economic policy’, the most likely outcome is that the new Greek government would in the end sign up for an equivalent austerity programme, a process similar to what happened in Ireland and Portugal recently. Greece would then have to rely on short-term funding to avoid a default on coupon payments and bonds redemptions in July and August. One can also envisage that the IMF or EU will give the opposition party the benefit of the doubt during the summer and provide Greece with a bridge loan. But there is no doubt that the turmoil would then be elevated.

June 30, 2011

Greece: what is next!

For those who are wondering what is next in the Greek tragedy a clear article from Socgen below explain the possible future scenarios.

June 29, 2011

Los Alamos nuclear alert

A raging wildfire is threatening to engulf the Los Alamos National Laboratory.

Los Alamos likely contains more nuclear weapons than any other facility in the world.

As if that weren't bad enough, AP notes:

The anti-nuclear watchdog group Concerned Citizens for Nuclear Safety, however, said the fire appeared to be about 3 1/2 miles from a dumpsite where as many as 30,000 55-gallon drums of plutonium-contaminated waste were stored in fabric tents above ground. The group said the drums were awaiting transport to a low-level radiation dump site in southern New Mexico.Later, Los Alamos confirmed the allegation:

Lab spokesman Steve Sandoval declined to confirm that there were any such drums currently on the property.

Lab officials at first declined to confirm that such drums were on the property, but in a statement early Tuesday, lab spokeswoman Lisa Rosendorf said such drums are stored in a section of the complex known as Area G. She said the drums contain cleanup from Cold War-era waste that the lab sends away in weekly shipments to the Waste Isolation Pilot Plant.The lab has called in a special team to test plutonium and uranium levels in the air as a "precaution".

She said the drums were on a paved area with few trees nearby and would be safe even if a fire reached the storage area. Officials have said it is miles from the flames.

Italian banks under pressure

Morgan Stanley is reporting an explanation on why recently Italian banks seem to be at the center of the interest of speculators. Italian banks are accounting for the three most active positions in Goldman's Dark Pool. For the second day in a row, the most actives continue to be UniCredit and Banca Monte dei Paschi di Siena (Intesa has fallen from 3rd to 12):

Morgan Stanley is reporting an explanation on why recently Italian banks seem to be at the center of the interest of speculators. Italian banks are accounting for the three most active positions in Goldman's Dark Pool. For the second day in a row, the most actives continue to be UniCredit and Banca Monte dei Paschi di Siena (Intesa has fallen from 3rd to 12): There are some speculations in the local papers that the disagreement between PM Berlusconi and Finance Minister Tremonti has reached a new peak again and that Tremonti may threaten to resign again and this time Berlusconi may be prepared to accept.

Given Mr Tremonti stronger reputation (and Berlusconi's weaker stance esp in the international community), if confirmed this is clearly not helpful for Italy especially at this very sensitive moment

The same papers also indicate that Bini Smaghi (who has to resign from his post as ECB board member given Draghi's appointment) could be appointed should Tremonti go (and he would be a well respected high level appoiontment)

None of this is confirmed and it is not obvious even whether Tremonti would resign, but the uncertainty in itself at a very difficult moment for the sovereign (and the already not very stable political situation in Italy) is not helpful for the market in my view. This comes after Moodys changed outlook for Italy to negative last week

We have seen macro funds (esp credit but also equity) effectively selling Italy since Friday (both on stand-lone concerns for the sovereign) but also as a way to position more negatively on Southern Europe

Italian banks have been significantly impacted recently and some show cheap values (ISP for example which is fully recap'd to 10% CT1 but trades below 0.8x NAV), but I would just be reluctant to get involved as yet as the situation unfolds in Italy but also in Southern Europe, as this is still very fluid. And I think the way bank stocks traded today (with Italians in the red in a green screen) tells me that investors are cautious too.

June 28, 2011

Greece austerity package

Below a full breakdown of the actual proposed fiscal measures to be implemented if the austerity vote passes tomorrow, courtesy of the BBC.

The plan involves cutting 14.32bn euros ($20.50bn; £12.82bn) of public spending, while raising 14.09bn euros in taxes over five years.

These are some of the austerity measures planned.

TAXATION

The plan involves cutting 14.32bn euros ($20.50bn; £12.82bn) of public spending, while raising 14.09bn euros in taxes over five years.

These are some of the austerity measures planned.

TAXATION

- Taxes will increase by 2.32bn euros this year, with additional taxes of 3.38bn euros in 2012, 152m euros in 2013 and 699m euros in 2014.

- A solidarity levy of between 1% and 5% of income will be levied on households to raise 1.38bn euros.

- The tax-free threshold for income tax will be lowered from 12,000 to 8,000 euros.

- There will be higher property taxes

- VAT rates are to rise: the 19% rate will increase to 23%, 11% becomes 13%, and 5.5% will increase to 6.5%.

- The VAT rate for restaurants and bars will rise to 23% from 13%.

- Luxury levies will be introduced on yachts, pools and cars.

- Some tax exemptions will be scrapped

- Excise taxes on fuel, cigarettes and alcohol will rise by one third.

- Special levies on profitable firms, high-value properties and people with high incomes will be introduced.

- The public sector wage bill will be cut by 770m euros in 2011, 600m euros in 2012, 448m euros in 2013, 300m euros in 2014 and 71m euros in 2015.

- Nominal public sector wages will be cut by 15%.

- Wages of employees of state-owned enterprises will be cut by 30% and there will be a cap on wages and bonuses.

- All temporary contracts for public sector workers will be terminated.

- Only one in 10 civil servants retiring this year will be replaced and only one in 5 in coming years.

- Defence spending will be cut by 200m euros in 2012, and by 333m euros each year from 2013 to 2015.

- Health spending will be cut by 310m euros this year and a further 1.81bn euros in 2012-2015, mainly by lowering regulated prices for drugs.

- Public investment will be cut by 850m euros this year.

- Subsidies for local government will be reduced.

- Education spending will be cut by closing or merging 1,976 schools.

- Social security will be cut by 1.09bn euros this year, 1.28bn euros in 2012, 1.03bn euros in 2013, 1.01bn euros in 2014 and 700m euros in 2015.

- There will be more means-testing and some benefits will be cut.

- The government hopes to collect more social security contributions by cracking down on evasion and undeclared work.

- The statutory retirement age will be raised to 65, 40 years of work will be needed for a full pension and benefits will be linked more closely to lifetime contributions.

- The government aims to raise 50bn euros from privatisations by 2015, including:

- Selling stakes this year in the betting monopoly OPAP, the lender Hellenic Postbank, port operators Piraeus Port and Thessaloniki Port as well as Thessaloniki Water.

- It has agreed to sell 10% of Hellenic Telecom to Deutsche Telekom for about 400m euros.

- Next year, the government plans to sell stakes in Athens Water, refiner Hellenic Petroleum, electricity utility PPC, lender ATEbank as well as ports, airports, motorway concessions, state land and mining rights.

- It plans further sales to raise 7bn euros in 2013, 13bn euros in 2014 and 15bn euros in 2015.

June 27, 2011

$20 billion air conditioning bill for US troops

Today, NPR reported a stunning story: Air conditioning in Iraq and Afghanistan costs $20.2 billion annually.

Today, NPR reported a stunning story: Air conditioning in Iraq and Afghanistan costs $20.2 billion annually.That’s more than NASA’s budget. It’s more than BP has paid so far for damage during the Gulf oil spill. It’s what the G-8 has pledged to help foster new democracies in Egypt and Tunisia.To power an air conditioner at a remote outpost in land-locked Afghanistan, a gallon of fuel has to be shipped into Karachi, Pakistan, then driven 800 miles over 18 days to Afghanistan on roads that are sometimes little more than “improved goat trails,” [retired Brigadier General Steven] Anderson says. “And you’ve got risks that are associated with moving the fuel almost every mile of the way.”

In 2010, the US spent $165.1 billion in Iraq and Afghanistan, according to the Congressional Research Service. This means roughly 12% of expenditures were on air conditioning.

Fuel is not only a budget breaker, it’s a logistical nightmare that can cost lives. Anderson, who manged operational logistics for Gen. David Patreaus in Iraq, explained the impacts of air conditioning on a commander:

“He literally has to stop his combat operations for two days every two weeks so he can go back and get his fuel. And when he’s gone, the enemy knows he’s gone, and they go right back to where they were before. He has to start his counter-insurgency operations right back at square one.”

Another downplayed nuclear accident: Fort Calhoun, Nebraska

A new hidden nuclear disaster could be in the making in Nebraska. It seems the situation at the Fort Calhoun, Nebraska nuclear power plant is getting of some concern. Missouri River flood waters have penetrated the last ditch water-filled wall, and have surrounded the containment buildings and other vital areas of a Nebraska nuclear plant.

As Reuters reports:

"The U.S. Nuclear Regulatory Commission (NRC) said the breach in the 2,000-foot (600 meters) inflatable berm around the Fort Calhoun station occurred around 1:25 a.m. local time. More than 2 feet (60 cm) of water rushed in around containment buildings and electrical transformers at the 478-megawatt facility located 20 miles (30 km) north of Omaha."

Naturally, the severity of the situation is being downplayed by the NRC, very much the way Tepco and Japanese authorities pretended the Fukushima situation was under control, until it was uncovered that there had been plant meltdown within hours of the tsunami: "Reactor shutdown cooling and spent-fuel pool cooling were unaffected, the NRC said. The plant, operated by the Omaha Public Power District, has been off line since April for refueling."

More from Reuters:

Crews activated emergency diesel generators after the breach, but restored normal electrical power by Sunday afternoon, the NRC said.

Buildings at the Fort Calhoun plant are watertight, the agency said. It noted that the cause of the berm breach is under investigation.

NRC Chairman Gregory Jaczko and other officials planned to visit the site on Monday.

Jaczko will also visit the Cooper Nuclear Station near Brownville, Nebraska, another facility that has been watched closely with Missouri River waters rising from heavy rains and snow melt.

As Reuters reports:

"The U.S. Nuclear Regulatory Commission (NRC) said the breach in the 2,000-foot (600 meters) inflatable berm around the Fort Calhoun station occurred around 1:25 a.m. local time. More than 2 feet (60 cm) of water rushed in around containment buildings and electrical transformers at the 478-megawatt facility located 20 miles (30 km) north of Omaha."

Naturally, the severity of the situation is being downplayed by the NRC, very much the way Tepco and Japanese authorities pretended the Fukushima situation was under control, until it was uncovered that there had been plant meltdown within hours of the tsunami: "Reactor shutdown cooling and spent-fuel pool cooling were unaffected, the NRC said. The plant, operated by the Omaha Public Power District, has been off line since April for refueling."

More from Reuters:

Crews activated emergency diesel generators after the breach, but restored normal electrical power by Sunday afternoon, the NRC said.

Buildings at the Fort Calhoun plant are watertight, the agency said. It noted that the cause of the berm breach is under investigation.

NRC Chairman Gregory Jaczko and other officials planned to visit the site on Monday.

Jaczko will also visit the Cooper Nuclear Station near Brownville, Nebraska, another facility that has been watched closely with Missouri River waters rising from heavy rains and snow melt.

Spanish banks' 50 billion hole

Bloomberg reported: "Spanish banks have 50 billion euros ($70.7 billion) in unrecognised problematic real estate assets, El Confidencial reported, citing a report by the Boston Consulting Group. The consulting group estimates that Spanish banks need between 20 billion euros and 30 billion euros in additional capital and that Spain’s bank rescue fund, known as the FROB, could end up taking over 20 percent of the banking industry, El Confidencial added." But not before the second European Stress Test finds that all Cajas, just like last year, are perfectly capitalized, in what will be the latest daily lie out of Europe.

Greece update: Default talks on the media scene

It seems that even before the crucial vote in Athens on Wednesday everyone is already convinced Greece will default, last week Alan Greenspan said in brilliant interview with Charlie Rose that Greece is doomed and today more influential voices are anticipating a default in the coming days.

It seems that even before the crucial vote in Athens on Wednesday everyone is already convinced Greece will default, last week Alan Greenspan said in brilliant interview with Charlie Rose that Greece is doomed and today more influential voices are anticipating a default in the coming days.The risk of contagion in the Eurozone and indeed a global financial contagion remains real. Peripheral European bond markets are under pressure again today with 10 year bond yields in Ireland rising to over 12.1% and to over 11.65% in Portugal.

European leaders are preparing for a default by Greece. The German finance minister, Wolfgang Schaeuble, said yesterday that Europe is preparing "for the worst".

George Soros, Chairman of Soros Fund Management and famous for breaking the Bank of England in 1992, has warned that "we are on the verge of an economic collapse which starts, let's say, in Greece but it could easily spread."

The 80-year-old investor said that the “financial system remains extremely vulnerable."

Soros added that "there are fundamental flaws that need to be corrected." The core flaw, says Soros, is that the euro is not backed by a political union or joint treasury, so when something goes wrong with a participating country, there is "no provision for correction."

Soros said that it is "probably inevitable" that highly indebted countries will be given a way to quit the euro.

A further obstacle to the bailout has been reported today as German constitutional court in Karlsruhe is about to commence hearings on a lawsuit contesting the legality of the Greek bailout.

As Athens News reports, "the suit was filed last July by a group of five Eurosceptics led by economist Joachim Starbatty. According to the plaintiffs, the financial help package for Greece runs contrary to article 125 of the EU Treaty - the so-called no-bailout clause - which does not allow the EU or a member state to undertake the responsibility of covering the debts of another member state."

In the meanwhile Greek savers are bracing for the worst and draining banks' accounts.

Today, as part of its Weekly Credit Outlook, Moody's issued for the first time a very stark warning that should the rate of attrition in domestic deposits persist, or accelerate, the results would be disastrous.

From Moody's:

Our discussions with rated Greek banks last week and public information lead us to estimate that private-sector customer deposit outflows in the banking system amount to around 8% since the beginning of 2011, which is a key credit negative for Greek banks. The potential for further deposit outflows constitutes a major liquidity risk for banks as depositor sentiment is affected by negative political developments and Greece’s capability for timely repayment of its debt obligations. We expect Greek banks to find it increasingly challenging to lower their dependence on ECB repo funding as deposit balances continue to decline.

Private-sector deposits have been declining since late 2009, while outflows in May and June accelerated, as shown in the exhibit below. Greece’s heated political tensions (government reshuffling and resistance to the new austerity package) and the uncertainties regarding the Troika’s (European Union, European Central Bank, and International Monetary Fund) commitment to continue funding support to Greece are driving deposits elsewhere.

And if push come to shovel and Greece should default the question would be how much and who is going to lose.

Some interesting articles today have been raising scary scenarios:

As Louise Story wrote in the NY Times,

“It’s the $616 billion question: Does the euro crisis have a hidden A.I.G.? No one seems to be sure, in large part because the world of derivatives is so murky. But the possibility that some company out there may have insured billions of dollars of European debt has added a new tension to the sovereign default debate... The looming uncertainties are whether these contracts — which insure against possibilities like a Greek default — are concentrated in the hands of a few companies, and if these companies will be able to pay out billions of dollars to cover losses during a default.” (Derivatives Cloud the Possible Fallout From a Greek Default)

June 26, 2011

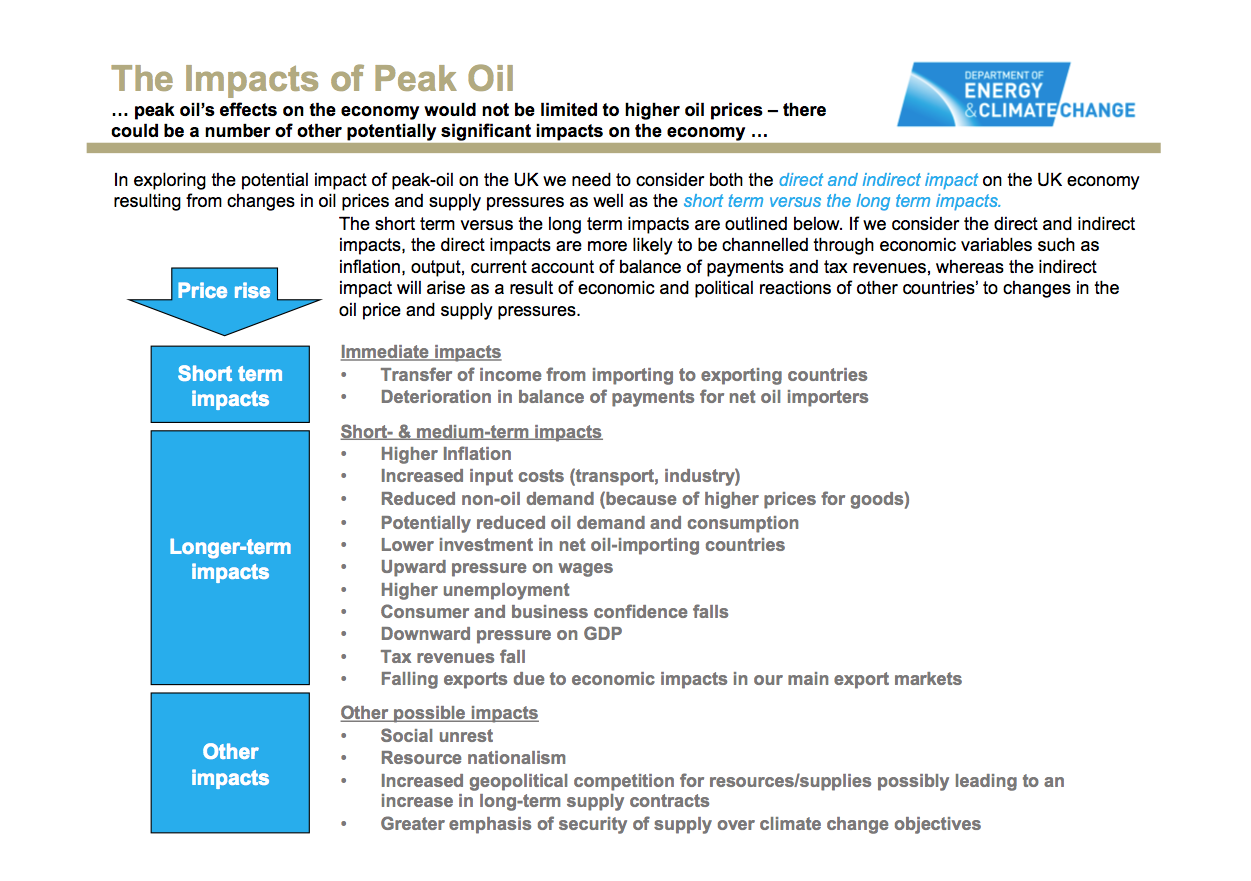

Peak Oil impact on the economy

The Guardian has released an internal UK government report on peak oil.

UK government 2 years ago ignored warnings about Peak Oil and played them down as alarmist and irrelevant. The report was eventually released under a Freedom of Information Act (FOIA) request:

Of the 17 bullet points on the slide, 16 have come to pass in the UK and in the neighbouring countries of Europe (click on slide to enlarge and open in separate window). Given that the research was conducted in 2007 and the report compiled in 2009, this conveys amazing insight.

Two important items are missing from the list and when these are taken on board, the story is complete.

1. Peak oil may threaten the global banking and financial system since the Ponzi scheme of growth based on credit expansion requires a growing stream of cheap energy to fuel the real economy. When the stream of cheap fuel dried up, the real economy failed, toppling the global fractional reserve banking system that lay at the heart of the Ponzi scheme. Fractional reserve banking has now been supplemented by Quantitative Easing as a means of creating money to drive consumption of finite reserves.

2. Peak oil will threaten pensions since these are based upon the excess net energy produced from high ERoEI energy sources (Energy Return on Energy Invested). As the ERoEI declines and the lifeblood of cheap net energy dries up, it is inevitable that society's ability to care for those not in work (young, old and dysfunctional) will be steadily eroded. This links to point 1 above via declining stock market valuations.

It seems that the global economy may be on the rocks again for the second time in three years, stemming from energy prices that society can ill afford to pay.

UK government 2 years ago ignored warnings about Peak Oil and played them down as alarmist and irrelevant. The report was eventually released under a Freedom of Information Act (FOIA) request:

Of the 17 bullet points on the slide, 16 have come to pass in the UK and in the neighbouring countries of Europe (click on slide to enlarge and open in separate window). Given that the research was conducted in 2007 and the report compiled in 2009, this conveys amazing insight.

Two important items are missing from the list and when these are taken on board, the story is complete.

1. Peak oil may threaten the global banking and financial system since the Ponzi scheme of growth based on credit expansion requires a growing stream of cheap energy to fuel the real economy. When the stream of cheap fuel dried up, the real economy failed, toppling the global fractional reserve banking system that lay at the heart of the Ponzi scheme. Fractional reserve banking has now been supplemented by Quantitative Easing as a means of creating money to drive consumption of finite reserves.

2. Peak oil will threaten pensions since these are based upon the excess net energy produced from high ERoEI energy sources (Energy Return on Energy Invested). As the ERoEI declines and the lifeblood of cheap net energy dries up, it is inevitable that society's ability to care for those not in work (young, old and dysfunctional) will be steadily eroded. This links to point 1 above via declining stock market valuations.

It seems that the global economy may be on the rocks again for the second time in three years, stemming from energy prices that society can ill afford to pay.

Greece and the Eurozone Russian Roulette

A key week is starting tomorrow for Greece and regardless of the decisions that will take place in Athens the situation in the Eurozone is deteriorating by the day.

The reality is that Greece should have defaulted in May 2010 and avoid an austerity torture that is destroying the country and dragging the Euro to hell.

Had the May 2010 deal provided for debt writedown, the Greek crisis would be over by now. The crises in Ireland and Portugal would probably have happened anyway but would have been easier to handle and the European sovereign debt market would surely be less fragile.

Greece, Ireland and Portugal are small countries and a major disaster can be averted if the debt meltdown can be confined to these three. But if Spain goes under, threatening next-in-line Italy, the world financial crisis will enter a new and potentially disastrous phase.

There is a dangerous divide in the Eurozone which has been getting bigger in the last years and is widening up rapidly. While Ireland has some hope to get out of this mess thanks to its offshore companies' production provided will be able to disentangle itself from the burden of the irish banking system; the situation is appalling in Spain, Greece and Italy.

On Friday, the yield on Irish 10-year bonds reached 12 per cent, the highest level yet seen, with Portugal not far behind. But more ominously, yields on Spanish 10-year bonds have been creeping up and reached 5.7 per cent on Friday.

Ten-year yields for Italy, Europe's largest bond market, have shot back up towards five per cent, close to the danger zone, and one of the ratings agencies (Moody's) has threatened a downgrade.

There is a high risk of accident in the Spanish or Italian bond markets, or of an unexpected bank failure or a government collapsing somewhere. On Friday, Bank of England governor Mervyn King put it: "Providing liquidity can only be used to buy time."

As for the ECB we are not sure if they are trying to save the situation or complicate it.

Last week's Irish edition of The Sunday Times, quoted an unnamed ECB official saying: "In the meantime, we may have to come to the conclusion that it doesn't really make sense for the ECB to keep putting €100bn into Irish banks. What we are doing is actually illegal, but we have being doing it because we want to help Ireland. Maybe we might come to the conclusion that we should stop."

Der Spiegel pointed out correctly:

If the rest of Europe abandons Greece, the crisis could spin out of control, spreading from one weak euro-zone country to the next. Investors would have no guarantees that Europe would not withdraw its support from Portugal or Ireland, if push came to shove, and they would sell their government bonds. The prices of these bonds would fall and risk premiums would go up. Then these countries would only be able to drum up fresh capital by paying high interest rates, which would only augment their existing budget problems. It's possible that they would no longer be able to raise any money at all, in which case they would become insolvent.

And the cash is running out fast, disturbing news last week on the liquidity of European banks is that the number of banks tendering for ECB liquidity surged to 353: higher by 118 from the week earlier as the liquidity contagion spreads, the highest since September 2008, when 371 banks were rushing to suckle at the ECB's teat.

In the meanwhile Labour Unions in Greece decided to cut another 0.15% from Greek GDP by doing absolutely nothing. As a result, as Athens News reports, "according to the General Confederation of Workers of Greece (GSEE) and the civil servants' umbrella federation Adedy, the 48-hour strike is an escalation of their recent industrial action comprising 24-hour nationwide strikes in protest of the medium-term programme. A main demonstration will be held on Tuesday, June 28, at the Pedion tou Areos park in central Athens at 11am, while on Wednesday another demonstration will be held in downtown Klafthmonos Square."

As a reminder June 28, is the far more critical Greece austerity vote, which unlike the vote of confidence already has several PASOK members saying they will vote against it.

This could explain why Le Figaro reports today that a working group of French banks led by BNP Paribas has proposed, and been agreed to by the French Treasury, that maturing debt would be rolled over into a a 30 year maturity piece, accounting for 50% of the total existing debt, and another 20% would go into a "zero coupon" fund focused on high quality stocks. Also according to Le Figaro, borrowings under the proposed scheme would pay an interest equivalent to what Greek "public" interest is plus a variable interest rate "likely to be linked to an economic Greek indicator such as GDP" (which being negative for years to come will likely means lower interest than prevailing).

The implied haircut for the Greek Treasury would be between 30% and 50%.

At least 30% of the rolling over debt would not come back to the issuing authority.

This funding avenue closure would commence the waterfall that triggers the liquidity cascade that culminate with every single European money market fund breaking the buck.

The reality is that Greece should have defaulted in May 2010 and avoid an austerity torture that is destroying the country and dragging the Euro to hell.

Had the May 2010 deal provided for debt writedown, the Greek crisis would be over by now. The crises in Ireland and Portugal would probably have happened anyway but would have been easier to handle and the European sovereign debt market would surely be less fragile.

Greece, Ireland and Portugal are small countries and a major disaster can be averted if the debt meltdown can be confined to these three. But if Spain goes under, threatening next-in-line Italy, the world financial crisis will enter a new and potentially disastrous phase.

There is a dangerous divide in the Eurozone which has been getting bigger in the last years and is widening up rapidly. While Ireland has some hope to get out of this mess thanks to its offshore companies' production provided will be able to disentangle itself from the burden of the irish banking system; the situation is appalling in Spain, Greece and Italy.

On Friday, the yield on Irish 10-year bonds reached 12 per cent, the highest level yet seen, with Portugal not far behind. But more ominously, yields on Spanish 10-year bonds have been creeping up and reached 5.7 per cent on Friday.

Ten-year yields for Italy, Europe's largest bond market, have shot back up towards five per cent, close to the danger zone, and one of the ratings agencies (Moody's) has threatened a downgrade.

There is a high risk of accident in the Spanish or Italian bond markets, or of an unexpected bank failure or a government collapsing somewhere. On Friday, Bank of England governor Mervyn King put it: "Providing liquidity can only be used to buy time."

As for the ECB we are not sure if they are trying to save the situation or complicate it.

Last week's Irish edition of The Sunday Times, quoted an unnamed ECB official saying: "In the meantime, we may have to come to the conclusion that it doesn't really make sense for the ECB to keep putting €100bn into Irish banks. What we are doing is actually illegal, but we have being doing it because we want to help Ireland. Maybe we might come to the conclusion that we should stop."

Der Spiegel pointed out correctly:

If the rest of Europe abandons Greece, the crisis could spin out of control, spreading from one weak euro-zone country to the next. Investors would have no guarantees that Europe would not withdraw its support from Portugal or Ireland, if push came to shove, and they would sell their government bonds. The prices of these bonds would fall and risk premiums would go up. Then these countries would only be able to drum up fresh capital by paying high interest rates, which would only augment their existing budget problems. It's possible that they would no longer be able to raise any money at all, in which case they would become insolvent.

And the cash is running out fast, disturbing news last week on the liquidity of European banks is that the number of banks tendering for ECB liquidity surged to 353: higher by 118 from the week earlier as the liquidity contagion spreads, the highest since September 2008, when 371 banks were rushing to suckle at the ECB's teat.

In the meanwhile Labour Unions in Greece decided to cut another 0.15% from Greek GDP by doing absolutely nothing. As a result, as Athens News reports, "according to the General Confederation of Workers of Greece (GSEE) and the civil servants' umbrella federation Adedy, the 48-hour strike is an escalation of their recent industrial action comprising 24-hour nationwide strikes in protest of the medium-term programme. A main demonstration will be held on Tuesday, June 28, at the Pedion tou Areos park in central Athens at 11am, while on Wednesday another demonstration will be held in downtown Klafthmonos Square."

As a reminder June 28, is the far more critical Greece austerity vote, which unlike the vote of confidence already has several PASOK members saying they will vote against it.

This could explain why Le Figaro reports today that a working group of French banks led by BNP Paribas has proposed, and been agreed to by the French Treasury, that maturing debt would be rolled over into a a 30 year maturity piece, accounting for 50% of the total existing debt, and another 20% would go into a "zero coupon" fund focused on high quality stocks. Also according to Le Figaro, borrowings under the proposed scheme would pay an interest equivalent to what Greek "public" interest is plus a variable interest rate "likely to be linked to an economic Greek indicator such as GDP" (which being negative for years to come will likely means lower interest than prevailing).

The implied haircut for the Greek Treasury would be between 30% and 50%.

At least 30% of the rolling over debt would not come back to the issuing authority.

This funding avenue closure would commence the waterfall that triggers the liquidity cascade that culminate with every single European money market fund breaking the buck.

Italy is rotting away: The Garbage Crisis in Naples

Many will remember how in 2008 the Garbage crisis won the headlines all over the world showing how Naples and its region was chocking under piles of uncollected rubbish.

Everyone was crying at that time the despicable situation and this crisis was one of the main reasons for the previous centre-left government going down and being replaced by the current one with Berlusconi as prime minister. Once in power Berlusconi promptly organized a media coverage of its successful intervention to quell the crisis and clean up the streets, in reality he simply hid the trash proverbially under the carpet by moving it to the rural areas and giving the impression of a mission accomplished. In reality this crisis was never solved, uncollected garbage has become part of the landscape now for 20 years but occasionally for political or business convenience was temporarily solved with the cooperation of the local mafia. Now that a former judge and arch-enemy of the Prime Minister has become the mayor of Naples suddenly the crisis is exploding again at new heights. Trash is again piling up on the streets of Naples and this time despite the gravity of the situation there is no mention of it on the foreign press, either they want to avoid further embarrassment and alarm on a country that is being targeted by rating agencies on his colossal debt and lack of productivity or simply there is no interest for a never-ending crisis that would have toppled down any other government in a matter of days everywhere else in the world.

If we want to look for a symbol of the state of a country I think there is none more powerful then this, a government unable to provide the most basic of services to its population. The message coming from Naples is that an entire country is rotting and not only in the sunny Naples while the government is fiddling.

To give an idea of the scale of the problem below some images from Naples:

For further details in English on the garbage emergency read here

Everyone was crying at that time the despicable situation and this crisis was one of the main reasons for the previous centre-left government going down and being replaced by the current one with Berlusconi as prime minister. Once in power Berlusconi promptly organized a media coverage of its successful intervention to quell the crisis and clean up the streets, in reality he simply hid the trash proverbially under the carpet by moving it to the rural areas and giving the impression of a mission accomplished. In reality this crisis was never solved, uncollected garbage has become part of the landscape now for 20 years but occasionally for political or business convenience was temporarily solved with the cooperation of the local mafia. Now that a former judge and arch-enemy of the Prime Minister has become the mayor of Naples suddenly the crisis is exploding again at new heights. Trash is again piling up on the streets of Naples and this time despite the gravity of the situation there is no mention of it on the foreign press, either they want to avoid further embarrassment and alarm on a country that is being targeted by rating agencies on his colossal debt and lack of productivity or simply there is no interest for a never-ending crisis that would have toppled down any other government in a matter of days everywhere else in the world.

If we want to look for a symbol of the state of a country I think there is none more powerful then this, a government unable to provide the most basic of services to its population. The message coming from Naples is that an entire country is rotting and not only in the sunny Naples while the government is fiddling.

To give an idea of the scale of the problem below some images from Naples:

For further details in English on the garbage emergency read here

June 19, 2011

UK banks running out of the Eurozone

An article from the Telegraph revealed today that UK banks are abandoning the Euro zone to protect their investments from the incoming collapse of Greece, another warning signal of the dismal situation in the Euro area and a clear signal of how the markets are convinced that all the reassurances of the ECB and EU are merely words not being supported by facts. Quite day on the Euro front this Sunday in preparation of the incoming storm next week.

Excerpt from The Telegraph:

Senior sources have revealed that leading banks, including Barclays and Standard Chartered, have radically reduced the amount of unsecured lending they are prepared to make available to eurozone banks, raising the prospect of a new credit crunch for the European banking system.

Excerpt from The Telegraph:

Senior sources have revealed that leading banks, including Barclays and Standard Chartered, have radically reduced the amount of unsecured lending they are prepared to make available to eurozone banks, raising the prospect of a new credit crunch for the European banking system.

Standard Chartered is understood to have withdrawn tens of billions of pounds from the eurozone inter-bank lending market in recent months and cut its overall exposure by two-thirds in the past few weeks as it has become increasingly worried about the finances of other European banks.

Barclays has also cut its exposure in recent months as senior managers have become increasingly concerned about developments among banks with large exposures to the troubled European countries Greece, Ireland, Spain, Italy and Portugal.

In its interim management statement, published in April, Barclays reported a wholesale exposure to Spain of £6.4bn, compared with £7.2bn last June, while its exposure to Italy has fallen by more than £100m.

One source said it was “inevitable” that British banks would look to minimise their potential losses in the event the eurozone crisis were to get worse. “Everyone wants to ensure that they are not badly affected by the crisis,” said one bank executive.

Moves by stronger banks to cut back their lending to weaker banks is reminiscent of the build-up to the financial crisis in 2008, when the refusal of banks to lend to one another led to a seizing-up of the markets that eventually led to the collapse of several major banks and taxpayer bail-outs of many more.

June 18, 2011

Italy downgrade looming

For those who want to know more on the real status of the Italian economy, I would reccomend reading the following report from SocGen:

How Vulnerable is Italy

Below Full text from Moody's:

Frankfurt am Main, June 17, 2011 -- Moody's Investors Service has today placed Italy's Aa2 local and foreign currency government bond ratings on review for possible downgrade, while affirming its short-term ratings at Prime-1.

The main drivers that prompted the rating review are:

(1) Economic growth challenges due to macroeconomic structural weaknesses and a likely rise in interest rates over time;

(2) Implementation risks surrounding the fiscal consolidation plans that are required to reduce Italy's stock of debt and keep it at affordable levels; and

(3) Risks posed by changing funding conditions for European sovereigns with high levels of debt.

Moody's review will evaluate the weight of these growing risks in light of the country's high rating but also relative to some credit-strengthening trends that have been observed in recent years and are expected over the coming years, such as improved fiscal governance, lower budget deficits and a modest economic recovery.

RATIONALE FOR REVIEW

First, the Italian economy faces growth challenges in an environment characterized by long-term structural impediments to growth and potentially rising interest rates. Structural economic weaknesses -- mainly low productivity and important labour and product market rigidities -- have been a major impediment to growth in the last decade and continue to hinder the economy's recovery from the severe recession it experienced in 2009. Italy has so far only recovered a fraction of the nearly seven percentage points in GDP that it lost during the global crisis, despite low interest rates, which are likely to rise in the medium term. Growth prospects for the Italian economy in the coming years will be a crucial factor that will determine the government's revenues and the achievement of fiscal consolidation targets.

Second, there are implementation risks to the fiscal consolidation plans that are required to reduce Italy's stock of public debt to more affordable levels. Against a backdrop of rising interest rates and weak economic growth, the government may find it difficult to generate the primary surpluses that are needed to place the public debt-to-GDP ratio and the interest burden on a solid downward trend. The adoption of additional conservative fiscal policies may prove more difficult in the near future because the current government's electoral support is weakening, with the government facing challenges in gaining public approval for its policies. For example, the government's recent energy and water supply proposals were rejected by popular vote.

Third, the fragile market sentiment that continues to surround European sovereigns with high levels of debt poses additional risks for Italy. The continued stability of market demand for Italy's debt is uncertain at current yields. Although future policy actions within the euro area could reduce investors' concerns and stabilize funding costs, the opposite is also possible. In any event, going forward, investors appear likely to differentiate more among euro area sovereign borrowers than they did prior to the financial crisis, to the disadvantage of euro area countries with higher-than-average debt burdens, like Italy.

FOCUS OF RATINGS REVIEW

Moody's review of Italy's sovereign rating will focus on the growth prospects for the Italian economy in coming years, and particularly the prospects for a removal of important structural bottlenecks that could hinder a stronger economic recovery in the medium term. The review will also examine the government's ability to achieve ambitious fiscal consolidation targets and to implement further plans to generate substantial primary surpluses in the medium term. This will include an analysis of the vulnerability of the Italian government debt trajectory to a rise in risk premia, as well as the options for the government to react. The government's new fiscal plan, which is expected to be announced shortly, will be considered during the review.

In addition, any broader developments across the euro area, in particular with regard to the resolution of the euro area debt crisis and its impact on funding costs, could be important determinants of the outcome of Moody's rating review

PREVIOUS RATING ACTION AND METHODOLOGY

Moody's last rating action affecting Italy was implemented on 15 May 2002, when the rating agency upgraded Italy's Aa3 government bond ratings to Aa2 with a stable outlook. The rating action prior to that was taken on 3 July 1996, when the rating agency upgraded Italy's A1 government bond ratings to Aa3.

June 15, 2011

Emigration visualized

Peoplemovin, an experimental project in data visualization by Carlo Zapponi, that shows the flows of 215,738,321 migrants as of 2010. The migration data provided by The World Bank is plotted as a flow chart that connects emigration and destination countries. The chart is split in two columns, the emigration countries on the left and the destination countries on the right. The thickness of the lines connecting the countries represents the amount of immigrated people and the color code from blue to red puts the countries in comparison to the rest of the world.

Online Education Infograph

Check out this infographic from OnlineEducation.net about how the world of online learning has changed and grown over the years.

![]()

Via: OnlineEducation.net

Via: OnlineEducation.net

June 14, 2011

The man who screwed an entire country

read the full article HERE

June 11, 2011

NATO´s Middle East Chess Game

Every good chess player knows that before striking the opponent you want to carefully position your pieces on the board and when ready then unleash hell.

NATO is playing the same game in North Africa and Middle East, toppling down every dictator and replacing it with a military junta as in Egypt with no clear leader and easy to be controlled and replaced if the case, they also get a democratic branding from the support of western countries together with a generous support package to keep things calm among the population.

The choice of countries is not casual, all of them have a strategic relevance either in oil production or logistics, as you can see below Egypt and Yemen are vital to oil supplies, Bahrain is vital to both oil production and logistics and Libya is a perfect replacement for oil from the Middle East should an Iranian blockade take place in Strait of Ormuz, the oil chockpoint where 50% of the world´s seaborne oil transits daily.

Libya has some of the biggest and most proven oil reserves -- 43.6 billion barrels -- outside Saudi Arabia, and some of the best drilling prospects. Libya's oil is unusually "sweet" and "light," fundamentally is high-quality crude oil providing a better value than Saudi one should supplies from the Arabian region be disrupted at any stage. And furthermore Libya is close to Europe making easier to transit oil to the European and American markets while avoiding any possible disruption when the situation in the Middle East will escalate.

No doubt that once that Libyan oil fields will be under NATO control and production will be re-established a new front of the New Resource War we entered into will be opened most probably directly on the Iranian borders.

Iran is well aware of this and since many years its government has been counteracting to the siege that is being undertaken on its borders. After all Iraq on the western border and Afghanistan on the eastern border are under US control, Saudi Arabia and the Gulf States on his southern border are close US Allies and hosting major military bases. Pakistan on his south eastern border is without leadership and in lack of control while allowing the CIA to do whatever they want on its territory included staging a farsical attack to Osama Bin Laden on the outskirts of their capital. The Iranian northern borders are with Turkey a close US ally and not a good friend of Iran and the Caucasus republics of Russia which aside from Azerbaijan are normally hostile to Iran, the only friendly border at least for now is the one with Turkmenistan which is also vital for Iranian exports to China and Central Asia.

When the tension with Iran will mount and if a full scale war will explode the first victim will be the economy, The Strait of Ormuz will be shut down immediately and oil prices will explode to historical heights, a new great depression will start and as a consequence demand destruction will allow to make up for the shortfalls in production. If NATO plans will succeed Middle East will become a large battlefield for the core resources we covet and we cannot live without. Strange world where you have to wish that a dictator like Gaddafi will live another day.

NATO is playing the same game in North Africa and Middle East, toppling down every dictator and replacing it with a military junta as in Egypt with no clear leader and easy to be controlled and replaced if the case, they also get a democratic branding from the support of western countries together with a generous support package to keep things calm among the population.

The choice of countries is not casual, all of them have a strategic relevance either in oil production or logistics, as you can see below Egypt and Yemen are vital to oil supplies, Bahrain is vital to both oil production and logistics and Libya is a perfect replacement for oil from the Middle East should an Iranian blockade take place in Strait of Ormuz, the oil chockpoint where 50% of the world´s seaborne oil transits daily.

Libya has some of the biggest and most proven oil reserves -- 43.6 billion barrels -- outside Saudi Arabia, and some of the best drilling prospects. Libya's oil is unusually "sweet" and "light," fundamentally is high-quality crude oil providing a better value than Saudi one should supplies from the Arabian region be disrupted at any stage. And furthermore Libya is close to Europe making easier to transit oil to the European and American markets while avoiding any possible disruption when the situation in the Middle East will escalate.

No doubt that once that Libyan oil fields will be under NATO control and production will be re-established a new front of the New Resource War we entered into will be opened most probably directly on the Iranian borders.

Iran is well aware of this and since many years its government has been counteracting to the siege that is being undertaken on its borders. After all Iraq on the western border and Afghanistan on the eastern border are under US control, Saudi Arabia and the Gulf States on his southern border are close US Allies and hosting major military bases. Pakistan on his south eastern border is without leadership and in lack of control while allowing the CIA to do whatever they want on its territory included staging a farsical attack to Osama Bin Laden on the outskirts of their capital. The Iranian northern borders are with Turkey a close US ally and not a good friend of Iran and the Caucasus republics of Russia which aside from Azerbaijan are normally hostile to Iran, the only friendly border at least for now is the one with Turkmenistan which is also vital for Iranian exports to China and Central Asia.

When the tension with Iran will mount and if a full scale war will explode the first victim will be the economy, The Strait of Ormuz will be shut down immediately and oil prices will explode to historical heights, a new great depression will start and as a consequence demand destruction will allow to make up for the shortfalls in production. If NATO plans will succeed Middle East will become a large battlefield for the core resources we covet and we cannot live without. Strange world where you have to wish that a dictator like Gaddafi will live another day.

Peak Oil alert gaining momentum

Since 2006, the international oil company TOTAL has consistently voiced warnings about the future inability of the oil industry to meet continued oil demand growth. In 2006, then CEO Thierry Desmarest stated that maximum oil production lies between 100 to 110 million b/d, reached potentially by 2020. Only a year later the new CEO Christophe de Margerie announced that it would be difficult for the industry to produce beyond 100 million b/d.

To summarize, according to TOTAL the world can likely not produce over 95 million barrels per day due to constraints in producing more technically challenging oil fields such as deepwater, heavy oil, and fields located in the arctic. Furthermore, such a production level is only possible if the countries in the Middle-East, especially Saudi-Arabia, Iran, and Iraq, will be able and willing to increase their production.

Ad when it comes to Saudi Arabia being able to increase production well the latest news are not encouraging:

From elEconomista.es (translation in English here)

The electricity company of Saudi Arabia warns that oil in this country could be depleted by 2030 if left unchecked domestic consumption. According to a report of Saudi Electric, domestic consumption is estimated to be between 2.5 and 3.4 million barrels a day.

The report, published in the magazine Al Mashka says that the increase in domestic consumption of oil is one of the main challenges facing the country, mainly because oil accounts for 80% of national income.

Abdel Salam al-Yamani, head of the Saudi Electricity Company also warned of the consequences for citizens to ignore the calls to save electricity and water, and has advised that they depend more on solar energy.

It appears the Saudi governement is well aware of this issue since on the 1st of June announced its intention to build 16 nuclear power plants which is quite ironic for a country supposedly full of oil.

From Reuters

DUBAI, June 1 (Reuters) - Saudi Arabia plans to build 16 nuclear power reactors by 2030 which could costs more than $100 billion, a Saudi-based newspaper reported on Wednesday, citing a top official.

The world's top crude exporter, Saudi is struggling to keep up with rapidly rising power demand. It has considered boosting its domestic energy capacity using nuclear reactors.

"After 10 years we will have the first two reactors," Abdul Ghani bin Melaibari, coordinator of scientific collaboration at King Abdullah City for Atomic and Renewable Energy, told Arab News.

Many have backed away from atomic plans after the accident at Japan's Fukushima Daiichi plant but oil-rich Gulf states are among the few countries looking to make major investments in nuclear power plants.

"After that, every year we will establish two, until we have 16 of them by 2030," he said.

The world's top crude exporter, Saudi is struggling to keep up with rapidly rising power demand. It has considered boosting its domestic energy capacity using nuclear reactors.

"After 10 years we will have the first two reactors," Abdul Ghani bin Melaibari, coordinator of scientific collaboration at King Abdullah City for Atomic and Renewable Energy, told Arab News.

Many have backed away from atomic plans after the accident at Japan's Fukushima Daiichi plant but oil-rich Gulf states are among the few countries looking to make major investments in nuclear power plants.

"After that, every year we will establish two, until we have 16 of them by 2030," he said.

CRUDE-OIL prices shot up on June 8th—Brent crude to a one-month high of $118.59 per barrel—after OPEC representatives meeting in Vienna were unable to reach an agreement on production quotas. Many had expected an increase in quotas as members with spare production capacity, led by Saudi Arabia, pushed to avoid a price spike that may dampen long-term demand. As figures released in BP’s "Statistical Review of World Energy" show, global oil production has struggled to keep up with increased demand recently, particularly from Asia. In China alone consumption has risen by over 4m barrels per day in the past decade, accounting for two-fifths of the global rise. In 2010 consumption exceeded production by over 5m barrels per day for the first year ever, as world oil stocks were run down.

Long-term consumption cannot exceed production. Even in short time frames, consumption can only exceed production if there is sufficient production in storage.

To cover 5 million barrels per day of excess consumption for a year, global oil stocks would have had to drop by 1.825 billion barrels. If that did not happen, we need another explanation.

Possible Explanations

Cheating (under-reporting production) by OPEC

Poor consumption numbers from China or elsewhere

Another source of production not shown

Some combination of the above

To cover 5 million barrels per day of excess consumption for a year, global oil stocks would have had to drop by 1.825 billion barrels. If that did not happen, we need another explanation.

Possible Explanations

Cheating (under-reporting production) by OPEC

Poor consumption numbers from China or elsewhere

Another source of production not shown

Some combination of the above

Regardless, it simply is not possible for oil consumption to grow faster than production for years on end.

June 8, 2011

46 years of proved oil reserves left

In its just released must read Statistical Review of World Energy, BP has many important observations.

From the report:

"World primary energy consumption – which this year includes for the first time a time series for commercial renewable energy – grew by 5.6% in 2010, the largest increase (in percentage terms) since 1973. Consumption in OECD countries grew by 3.5%, the strongest growth rate since 1984, although the level of OECD consumption remains roughly in line with that seen 10 years ago. Non-OECD consumption grew by 7.5% and was 63% above the 2000 level. Consumption growth accelerated in 2010 for all regions, and growth was above average in all regions. Chinese energy consumption grew by 11.2%, and China surpassed the US as the world’s largest energy consumer. Oil remains the world’s leading fuel, at 33.6% of global energy consumption, but oil continued to lose market share for the 11th consecutive year." And in terms of production reserves: "World proved oil reserves in 2010 were sufficient to meet 46.2 years of global production, down slightly from the 2009 R/P ratio because of a large increase in world production; global proved reserves rose slightly last year. An increase in Venezuelan official reserve estimates drove Latin America’s R/P ratio to 93.9 years – the world’s largest, surpassing the Middle East."

There is much more in the full report, but three charts bear a simple conclusion, crude prices likely have a long way to go up unless the global economy promptly commences another 2008 mega deflationary episode (read economic crisis).

Reserves-to-production (R/P) ratios:

And Real crude Prices since the Pennsylvania Oil Boom:

World trade movements of crude:

And the full booklet:

2030 Energy Outlook Booklet

From the report:

"World primary energy consumption – which this year includes for the first time a time series for commercial renewable energy – grew by 5.6% in 2010, the largest increase (in percentage terms) since 1973. Consumption in OECD countries grew by 3.5%, the strongest growth rate since 1984, although the level of OECD consumption remains roughly in line with that seen 10 years ago. Non-OECD consumption grew by 7.5% and was 63% above the 2000 level. Consumption growth accelerated in 2010 for all regions, and growth was above average in all regions. Chinese energy consumption grew by 11.2%, and China surpassed the US as the world’s largest energy consumer. Oil remains the world’s leading fuel, at 33.6% of global energy consumption, but oil continued to lose market share for the 11th consecutive year." And in terms of production reserves: "World proved oil reserves in 2010 were sufficient to meet 46.2 years of global production, down slightly from the 2009 R/P ratio because of a large increase in world production; global proved reserves rose slightly last year. An increase in Venezuelan official reserve estimates drove Latin America’s R/P ratio to 93.9 years – the world’s largest, surpassing the Middle East."

There is much more in the full report, but three charts bear a simple conclusion, crude prices likely have a long way to go up unless the global economy promptly commences another 2008 mega deflationary episode (read economic crisis).

Reserves-to-production (R/P) ratios:

And Real crude Prices since the Pennsylvania Oil Boom:

World trade movements of crude:

And the full booklet:

2030 Energy Outlook Booklet

A World of Debt

I have collected few interesting graphs on the debt crisis unfolding.This New York Times graphic did an excellent job of summing everything up:

(Source - click to view larger graphic at source)

(Source - click to view larger graphic at source)

If everybody owes everybody else, then kicking the can down the road only works if there's more wealth, more growth, and sufficient economic activity down that road to service the past debts.

It means that unless recovery and substantial growth are going to manifest soon we are going one bailout after the other to plunge the economy in a vicious death spiral.

When all of the most indebted countries are stacked up, we see that all but Russia carry a total indebtedness greater than 100% of GDP and that nine are carrying debt levels higher than any that have ever been repaid historically.

(Source)

(Source)

Note: 260% debt-to-GDP is the all time record for repayment, accomplished by England between 1815 and 1900, but required both massive cuts in spending and an industrial revolution.

Of course, debt is only one component of the story; there are also liabilities to consider. The above chart merely graphs the legally defined debts involved. If we bother to add back in the liability components, which are pensions, social security and government medical plans, the predicament is seen to be three to six times larger:

It means that unless recovery and substantial growth are going to manifest soon we are going one bailout after the other to plunge the economy in a vicious death spiral.

When all of the most indebted countries are stacked up, we see that all but Russia carry a total indebtedness greater than 100% of GDP and that nine are carrying debt levels higher than any that have ever been repaid historically.

Note: 260% debt-to-GDP is the all time record for repayment, accomplished by England between 1815 and 1900, but required both massive cuts in spending and an industrial revolution.

Of course, debt is only one component of the story; there are also liabilities to consider. The above chart merely graphs the legally defined debts involved. If we bother to add back in the liability components, which are pensions, social security and government medical plans, the predicament is seen to be three to six times larger:

Greece Industrial Production in free-fall

Given the daily protests on the streets of Athens and its austerity measures it is hardly surprising thatthe entire country is practically grinding to a halt with the Greek Industrial Production dropping by 11%.

Mining fell by 6.4pc, manufacturing decreased by 11.3pc, electricity production dropped 12.2pc, while the water supply declined by 6.8pc. Hard to imagine any recovery in this situation.

As for that bailout, even that is no longer certain, the indebted nation is expected to need more help in coming years, with estimates putting the sum at up to €100bn on top of an EU/IMF package granted last year worth €110bn.

Yesterday, the German business daily Handelsblatt quoted a "high-ranking European diplomatic source" who said that approval of a second rescue plan for Greece might be delayed because of resistance within the 17-nation eurozone.

We can easily expect comparable economic data out of the other PIIGS shortly.

Mining fell by 6.4pc, manufacturing decreased by 11.3pc, electricity production dropped 12.2pc, while the water supply declined by 6.8pc. Hard to imagine any recovery in this situation.

As for that bailout, even that is no longer certain, the indebted nation is expected to need more help in coming years, with estimates putting the sum at up to €100bn on top of an EU/IMF package granted last year worth €110bn.

Yesterday, the German business daily Handelsblatt quoted a "high-ranking European diplomatic source" who said that approval of a second rescue plan for Greece might be delayed because of resistance within the 17-nation eurozone.

We can easily expect comparable economic data out of the other PIIGS shortly.

June 7, 2011

{kind=link}

June 6, 2011

Castilla-La Mancha region on the edge of Bankruptcy

The Regional Secretary of the PP Vicente Tirado has described the situation as one of total bankruptcy.

The Junta de Comunidad de Castilla-La Mancha has more than 2000 million euros in unpaid invoices and 7000 million euros of debt, this situation is not only causing the impossibility to pay over 70,000 employees starting from next month but it is also bringing to ruin many small and medium enterprises in the region.

They are trying to scramble an emergency package of measures including privatization of the public television.

Those who can read Spanish may wish to consider reading the following article: El PP asegura que no hay dinero para pagar nóminas en Castilla-La Mancha

June 5, 2011

G7 facing High Risk of short-term energy shortages

Index 2011") An interesting new research evaluates the state of worldwide energy security.

An interesting new research evaluates the state of worldwide energy security.The G7 economies of France, Germany, Italy, Japan, UK and USA according to the study are at ‘high risk’ in the short-term, whilst China and countries from the oil producing MENA region are highlighted as facing increasing challenges in the future.

The Energy Security (short-term) Index has been developed by Maplecroft to identify the countries most vulnerable to shocks in energy supplies and price fluctuations in the international market on timescale of days to months. It assesses immediate risks to the availability, affordability and continuity of energy supplies in 196 countries by evaluating energy imports, diversity of supplies, import security and energy costs.

Only three countries, Sierra Leone (1), Gambia (2) and Guinea Bissau (3), are categorised as ‘extreme risk’ in the short-term index. However, a further 122 nations are rated ‘high risk,’ including the G7 economies of Italy (13), Japan (73), UK (90), Germany (104), France (107) and the USA (112).

Recent instability in the MENA region and the impact of increased crude oil prices has highlighted the dangers of an economy heavily dependent on imported fuels from a specific region. “Rising fuel prices in response to the political turmoil in the MENA region in early 2011 have shown that energy security is of paramount importance,” states Maplecroft CEO, Alyson Warhurst. “Many countries are greatly reliant on imported oil and gas from these regimes. In order to support economic growth and energy demands, they will need to diversify energy supplies by increasing import partners and expanding domestic production and renewable energy sources.”

World wealth levels

The next chart is rather self-explanatory. The richest nations, with wealth in 2010 above USD 100,000 per adult, are found in North America, Western Europe, and among the rich Asian-Pacific and Middle East countries. They are topped by Switzerland, Norway, Australia, Singapore and France, each of which records wealth per adult above USD 250,000. Average wealth in other major economies such as the USA, Japan, the United Kingdom and Canada also exceeds USD 200,000.

Interesting to see how Mexico, Brasil and Chile are rapidly growing and how India despite his stellar growth is still showing wealth levels comparable to Central Africa.

June 4, 2011

Fukushima new radioactive alert at reactor 1

The latest news from Japan are clearly confirming that this crisis regardless of the cover up of the media, TEPCO and Japanese government is very far from over.

From The Japan Times:

Tepco said today (Saturday the 4th) it has detected radiation of up to 4,000 millisieverts per hour at the building housing the No. 1 reactor at the Fukushima No. 1 nuclear plant.

The radiation reading, which was taken when Tokyo Electric Power Co. sent a robot into the No. 1 reactor building on Friday, is believed to be the largest detected in the air at the plant so far.

On Friday, Tepco found that steam was spewing from the reactor floor. Nationally televised news Saturday showed blurry video of steady smoke curling up from an opening in the floor.

Tepco has said radioactive water could start overflowing from temporary storage areas on June 20, or possibly sooner if there is heavy rainfall.

Two of the 370 tanks were due to arrive Saturday from a manufacturer in nearby Tochigi Prefecture, Tepco said. Two hundred of them can store 100 tons, and 170 can store 120 tons.

The tanks will continue arriving through August and will store a total of 40,000 tons of radioactive water, according to Tepco.

Nuclear fuel rods are believed to have melted almost completely and sunk to the bottom of three reactors' containers, although falling short of a complete meltdown, in which case the fuel would have melted entirely through the container bottoms.

Tepco has promised to bring the plant under control by January, but doubts are growing whether this projection is overly optimistic. The plan calls for a reprocessing system for the radioactive water by June 15, with hopes of reusing the water as coolant in the reactors.

From The Japan Times:

Tepco said today (Saturday the 4th) it has detected radiation of up to 4,000 millisieverts per hour at the building housing the No. 1 reactor at the Fukushima No. 1 nuclear plant.

The radiation reading, which was taken when Tokyo Electric Power Co. sent a robot into the No. 1 reactor building on Friday, is believed to be the largest detected in the air at the plant so far.

On Friday, Tepco found that steam was spewing from the reactor floor. Nationally televised news Saturday showed blurry video of steady smoke curling up from an opening in the floor.

Tepco has said radioactive water could start overflowing from temporary storage areas on June 20, or possibly sooner if there is heavy rainfall.

Two of the 370 tanks were due to arrive Saturday from a manufacturer in nearby Tochigi Prefecture, Tepco said. Two hundred of them can store 100 tons, and 170 can store 120 tons.

The tanks will continue arriving through August and will store a total of 40,000 tons of radioactive water, according to Tepco.

Nuclear fuel rods are believed to have melted almost completely and sunk to the bottom of three reactors' containers, although falling short of a complete meltdown, in which case the fuel would have melted entirely through the container bottoms.

Tepco has promised to bring the plant under control by January, but doubts are growing whether this projection is overly optimistic. The plan calls for a reprocessing system for the radioactive water by June 15, with hopes of reusing the water as coolant in the reactors.

June 3, 2011

The New Great Depression

Recently more and more important voices are ringing the alarm bell of a new recession coming although this time some of them do not hesitate to call it a new Depression.

No doubt that recent quantitative easings and government interventions are having the only purpouse of earning some time to avoid a sharp collapse, practically they are trying to drive us down a rolling hill instead of falling down a cliff. If this earned time would have been spent to seriously reform the economy, ban the derivatives and go back to a productive system would have been a wise decision, instead it has been used to reinflate myriad of bubbles while going on living like there is no tomorrow and not addressing any of the systemic risks that are growing by the day.

The most interesting graph that I have been checking constantly since 2008 and that give a clear picture of what is going on is the following:

Job losses have mounted faster and sharper than ever before while job recovery is non-existent; we are on a plateau and unfortunately in the following months we could slide down even more.

It is no wonder that many are starting to talk openly of Great Depression.

The news that frequent CNBC guest Peter Yastrow of Yastrow Origer (and formerly with DT Trading) told CNBC that "We’re on the verge of a great, great depression. The [Federal Reserve] knows it" went viral.

Although this is hardly any news since in the last 2 years the following experts have said that the economic crisis could be worse than the Great Depression:

In the meanwhile a new report from Moody's has just confirmed that as in regards to banks we are already far worse than during the Great Depression:

California is issuing IOUs for only the second time since the Great Depression.

Things haven't been this bad for state and local governments since the 30s and for common people will be even worst when soon normal services including food stamps in US will be terminated due to lack of funds. If everything goes according to tradition we could see a new crisis exploding in September before the US presidential election, last time in 2008 it changed the race to the White House in favour of Obama, this time it could sign his demise.

No doubt that recent quantitative easings and government interventions are having the only purpouse of earning some time to avoid a sharp collapse, practically they are trying to drive us down a rolling hill instead of falling down a cliff. If this earned time would have been spent to seriously reform the economy, ban the derivatives and go back to a productive system would have been a wise decision, instead it has been used to reinflate myriad of bubbles while going on living like there is no tomorrow and not addressing any of the systemic risks that are growing by the day.

The most interesting graph that I have been checking constantly since 2008 and that give a clear picture of what is going on is the following:

Job losses have mounted faster and sharper than ever before while job recovery is non-existent; we are on a plateau and unfortunately in the following months we could slide down even more.

It is no wonder that many are starting to talk openly of Great Depression.

The news that frequent CNBC guest Peter Yastrow of Yastrow Origer (and formerly with DT Trading) told CNBC that "We’re on the verge of a great, great depression. The [Federal Reserve] knows it" went viral.

Although this is hardly any news since in the last 2 years the following experts have said that the economic crisis could be worse than the Great Depression:

- Fed Chairman Ben Bernanke

- Former Fed Chairman Alan Greenspan (and see this and this)

- Former Fed Chairman Paul Volcker

- Economics scholar and former Federal Reserve Governor Frederic Mishkin

- The head of the Bank of England Mervyn King

- Nobel prize winning economist Joseph Stiglitz

- Nobel prize winning economist Paul Krugman

- Former Goldman Sachs chairman John Whitehead

- Economics professors Barry Eichengreen and and Kevin H. O'Rourke (updated here)

- Investment advisor, risk expert and "Black Swan" author Nassim Nicholas Taleb

- Well-known PhD economist Marc Faber

- Morgan Stanley’s UK equity strategist Graham Secker

- Former chief credit officer at Fannie Mae Edward J. Pinto

- Billionaire investor George Soros

- Senior British minister Ed Balls

In the meanwhile a new report from Moody's has just confirmed that as in regards to banks we are already far worse than during the Great Depression:

The most recent rate of bank charge offs, which hit $45 billion in the past quarter, and have now reached a total of $116 billion, is at 3.4%, which is substantially higher than the 2.25% hit in 1932, before peaking at at 3.4% rate by 1934.States and cities all over United States are in dire financial straits, and many may default in 2011.

California is issuing IOUs for only the second time since the Great Depression.

Things haven't been this bad for state and local governments since the 30s and for common people will be even worst when soon normal services including food stamps in US will be terminated due to lack of funds. If everything goes according to tradition we could see a new crisis exploding in September before the US presidential election, last time in 2008 it changed the race to the White House in favour of Obama, this time it could sign his demise.

Moody's downgrade Greece to junk level

It seems Greece is willing to begin criminal proceedings against Moody's after the latest downgrade to junk status.